*I am now posting as a regular contributor at Macrobusiness under the alias Rumplestatskin. I will be posting copies of posts at both websites for the coming weeks.

Hands up who knew that Australia avoided a technical recession in the aftermath of the GFC? Kevin Rudd certainly got some miles out of it, noting in his farewell speech how proud he was of that fact and the role his government played. But as usual all is not what it seems. The Keynesians shouldn’t be celebrating just yet, as Professor Tony Makin explains:

In the aftermath of the GFC in September 2008, Australia’s nominal GDP, real GDP measured on an income basis and on a production basis, as well as real GDP per person, all fell over two successive quarters, as did various other national income measures that account for the slump in export commodity prices (or terms of trade) at the time.Of the many national accounts series the Australian Bureau of Statistics publish, the only one indicating there wasn’t a recession was the real, or price level adjusted, national expenditure series.In the US, a recession dating committee of the National Bureau of Economic Research uses a battery of macro-economic measures, not just the somewhat arbitrary two successive quarters of negative real GDP.If the behaviour of Australia’s business cycle in the aftermath of the GFC had been assessed by an independent committee of economists with reference to a broader range of macroeconomic indicators in this way, a recession, albeit mild, would most likely have been declared for 2008-09.

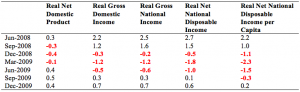

In his more technical analysis of the impact of fiscal stimulus, Professor Makin kindly summarises some of the other key measures in the National Accounts (in the below table), and notes the following:

Though routinely ignored in economic commentary, the real gross and net domestic and national income series are especially important measures of Australia’s international macroeconomic performance because they reflect the impact of the terms of trade (or ratio of prices received for exports to prices paid for imports) on the economy.Other notable recession features included declining total hours worked (for 5 straight quarters in the market sector), falling compensation to employees and increased unemployment.

But what is most interesting from the good professor’s analysis is the delay he observes between the recession and the appearance of fiscal stimulus in the data. He finds that:

Federal public investment actually contributed negatively to total expenditure over the critical December 2008 and March 2009 quarters, being -0.2 and -0.1 respectively, as did public investment by State and Local governments. As a result of administrative delays in implementing infrastructure spending, total public spending did increase by the end of 2009, but only after the worst of the GFC had passed, and then arguably crowded out private investment spending at the time.

Now there are obviously administrative delays to get $40billion spent on school halls and home insulation (not so much with cash handouts), but this very practical aspect of such Keynesian intervention must be addressed – how can governments time economic stimulus measures appropriately unless they have perfect foresight?

Professor Makin argues that the drop in the value of the Aussie dollar, and interest rate adjustments, are what ‘saved’ us from a technical recession, and not the delayed fiscal spending. Not only that, but government spending ramped up just as the private sector was itself recovering from the downturn, arguably crowding out private investment (although I personally wouldn’t suggest this is a major factor).

No comments:

Post a Comment